Paystack launched a new AI-powered dashboard today, marking the first major redesign of its merchant dashboard in ten years. More than 300,000 businesses now use Paystack to process trillions of naira monthly across five African countries, including Nigeria, Ghana, and South Africa.

The rebuild comes five months after the fintech announced major changes to its organisational structure with the creation of The Stack Group, a holding company to oversee its expansion beyond financial services.

“We’re not moving away from financial technology. We’re expanding our scope. Emerging technologies could include AI or stablecoins. The mandate is to solve both fintech and non-fintech problems that are critical to Africa’s digital future and development,” COO Amandine Lobelle said about the change.

At the time, the company also disclosed that it had become profitable, a milestone that arrived amid increasing pressure on African startups to demonstrate sustainable growth after years of venture capital-fuelled expansion.

The timing of the dashboard redesign is significant when viewed against the realities of the markets Paystack serves. Across Africa, the vast majority of businesses — often more than 80% in some countries — are small and informal operations whose owners rely heavily on smartphones to run day-to-day operations, from customer communication to inventory management.

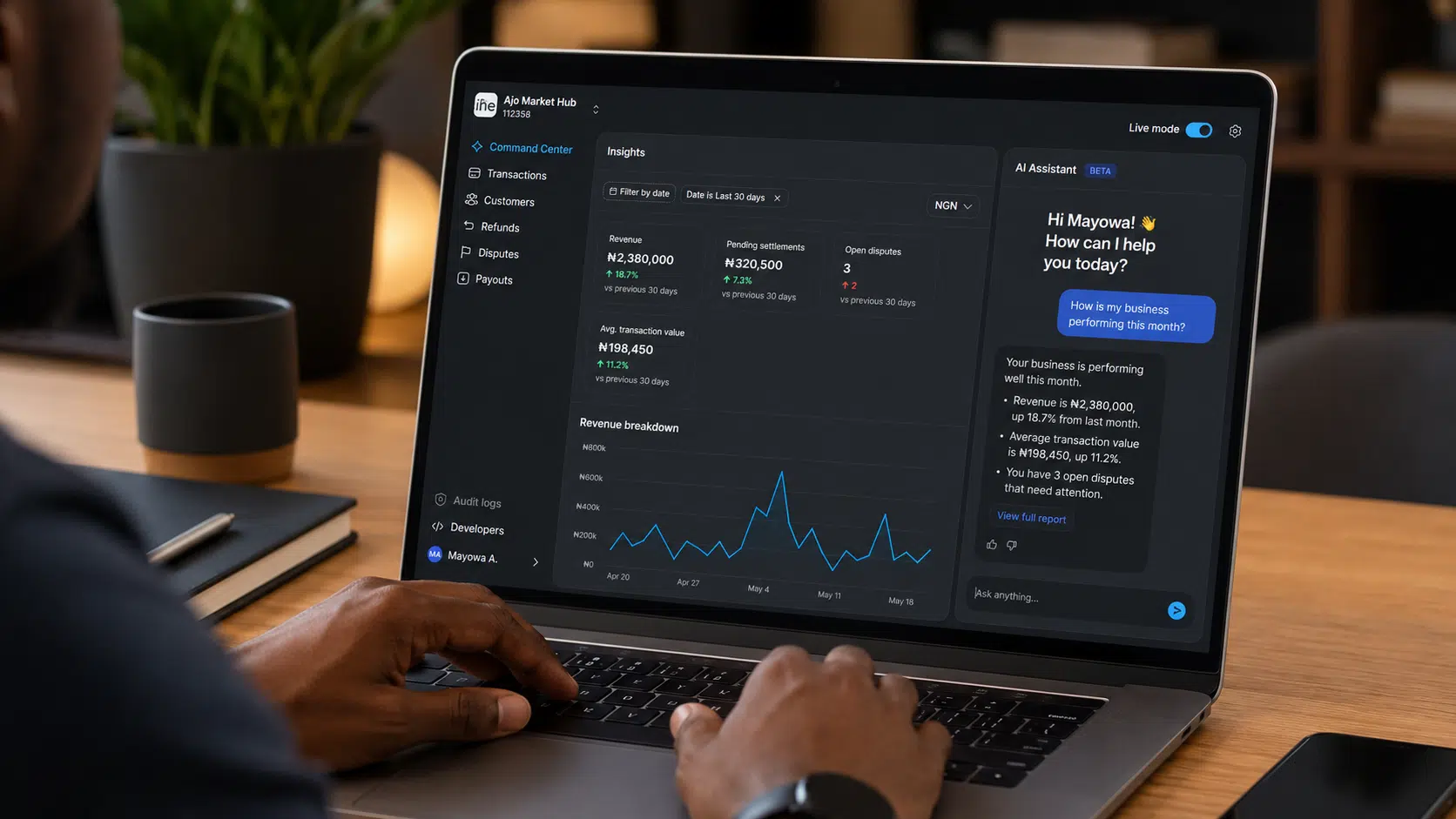

Over the years, Paystack’s dashboard has evolved into a more powerful product as the company has introduced additional payment options, analytics tools, settlement features, and integrations. However, that evolution also introduced complexity for merchants, who were often less interested in navigating multiple workflows and more focused on quickly understanding the health of their businesses.

The rebuilt dashboard is designed to simplify that experience. One of its most notable features allows merchants to ask plain-language questions about their payment data and receive responses in tables, charts, or written summaries.

“As with all things that we do at Paystack, it’s really just from listening to our merchants, understanding what works for them, what they need right now, and the challenges they’re facing,” Dara Assim-Ita, senior product designer at Paystack, says.

According to Assim-Ita, merchants’ needs have evolved beyond simply checking daily revenue figures. Increasingly, businesses want to understand why certain trends are happening, which customer segments are driving growth, or what operational changes might be affecting transaction performance.

Victoria Fakiya – Senior Writer

Techpoint Digest

Stop struggling to find your tech career path

Discover in-demand tech skills and build a standout portfolio in this FREE 5-day email course

“Merchants can now simply ask, ‘What happened with this transaction?’ or ‘Why is revenue down this week?’ and get a direct answer. The goal is to make the dashboard feel less like a static reporting tool and more like an intelligent command centre —one that helps merchants understand what’s happening, find what they need faster, and make better decisions,” Assim-Ita shares.

Businesses rapidly embracing artificial intelligence

The rise of artificial intelligence has emerged as one of the defining business and technology developments of the past three years. What was once considered a niche area of interest within technical communities has rapidly become a boardroom priority, with executives increasingly exploring how AI can drive operational efficiency, product innovation, and long-term competitiveness.

This shift is also becoming evident across Africa’s corporate landscape. According to McKinsey research, more than 40% of organisations on the continent are either experimenting with generative AI or have already implemented significant AI-driven solutions. While global conversations around artificial intelligence often centre on large language models, frontier research, and infrastructure, discussions in Africa are more closely tied to practical business applications.

Companies are increasingly focused on how AI can improve financial services, logistics, customer engagement, and internal processes, rather than on the underlying technology itself.

In January, as Paystack announced the formation of The Stack Group, it noted that artificial intelligence would play a central role in its future direction. The group’s subsidiary, TSG Labs, was specifically established to experiment with AI-led products while insulating Paystack’s core financial services business from potential regulatory risks associated with emerging technologies.

The new dashboard appears to be one of the earliest public expressions of that strategy. Paystack says it leveraged OpenAI models while building custom data retrieval and visualisation systems internally. To support the experience, the company developed a new internal service, Project Canvas API, which manages conversations, connects to model providers, and interfaces with Paystack’s existing systems.

The company says the architecture was designed to ensure that responses are grounded in actual merchant data rather than generated arbitrarily. Responses are also screened against safety and compliance requirements before being returned to users. Ahead of launch, the company conducted extensive adversarial testing and built a deterministic harness to improve consistency and reduce the likelihood of inaccurate outputs.

Despite growing global enthusiasm around artificial intelligence, many African businesses remain cautious about integrating the technology into their workflows. Yet executives across the ecosystem increasingly acknowledge that waiting too long may create its own disadvantages.

Nigerian fintechs are already integrating artificial intelligence into core operational workflows. Lending infrastructure provider Lendsqr, for instance, has said it uses AI-driven systems to support lending decisions, including analysis of customer voice and facial data.

This trend is also recognised at a regulatory level. A Central Bank of Nigeria (CBN) report shows that fintechs across the country are deploying AI for fraud detection, customer service automation, and credit scoring.

Assim-Ita notes that while caution around AI adoption is understandable, businesses need to begin experimenting now in order to understand how the technology can fit into their operations over time.

“The caution makes some sense, but we need to start testing slowly because over time, it’s going to become inevitable.”